UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☒

Filed by a party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Pursuant to Section 240.14a-12 |

EVERCORE INC.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than The Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11 |

[COVER E-MAIL]

I hope that this finds you well. I am the General Counsel of Evercore and I am reaching out because we recently filed our proxy. As part of this, we are asking shareholders to approve an additional 5 million shares under our plan. We make these requests periodically to ensure we have the capacity to continue to operate our business and execute on our growth strategy. As the equity plan is critical to the operation of our business, we want to highlight the following points and provide you with the attached deck, which contains additional information regarding our equity plan and compensation model.

| • | In 2025, we delivered the strongest revenue performance in our history, achieving record net revenues. This strong performance reflects the investments we have made in our people and capabilities, which are the primary drivers of growth in our business. |

| • | Equity compensation is a deliberate investment in our business. As a human capital–driven firm, our ability to recruit, retain and motivate high-performing, revenue-generating professionals is critical to delivering long-term shareholder value. Equity enables multi-year retention and alignment with shareholders in a way that cash compensation does not replicate. |

| • | We have been disciplined in how we use equity and have actively managed our capital return and share repurchase programs to offset the dilutive impact of equity compensation programs, achieving a negative net burn rate over the past three years. |

| • | Without a meaningful equity reserve, we would have to consider increasing our use of cash-based compensation, which would reduce available cash, including for repurchases, and be less effective at aligning employee and shareholder interests. |

| • | We are requesting an additional 5 million shares to provide greater certainty for the long-term management of our compensation program and strategic growth. |

We would greatly appreciate your support for this proposal. We know this is peak proxy season, but we would appreciate the opportunity to discuss our request further with you on a call.

Thank you for your time and consideration of this matter.

Evercore 2026 Equity Plan Proposal May 2026

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, which reflect our current views with respect to, among other things, our operations and financial performance. In some cases, you can identify these forward-looking statements by the use of words such as “outlook”, “backlog” “believes”, “expects”, “potential”, “probable”, “continues”, “may”, “will”, “should”, “seeks”, “approximately”, “predicts”, “intends”, “plans”, “estimates”, “anticipates” or the negative versions of these words or other comparable words. All statements other than statements of historical fact included in this presentation are forward- looking statements and are based on various underlying assumptions and expectations and are subject to known and unknown risks, uncertainties and assumptions, and may include projections of our future financial performance based on our growth strategies and anticipated trends in our business. Such forward-looking statements are subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. We believe these factors include, but are not limited to, those described under “Risk Factors” discussed in our Annual Report on Form 10-K for the year ended December 31, 2025 and subsequent Quarterly Reports on Form 10-Q and current reports filed under Form 8-K. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this discussion. In addition, new risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Accordingly, you should not rely upon forward-looking statements as a prediction of actual results and we do not assume any responsibility for the accuracy or completeness of any of these forward-looking statements. We undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise. Please note this presentation is available at www.evercore.com. 1

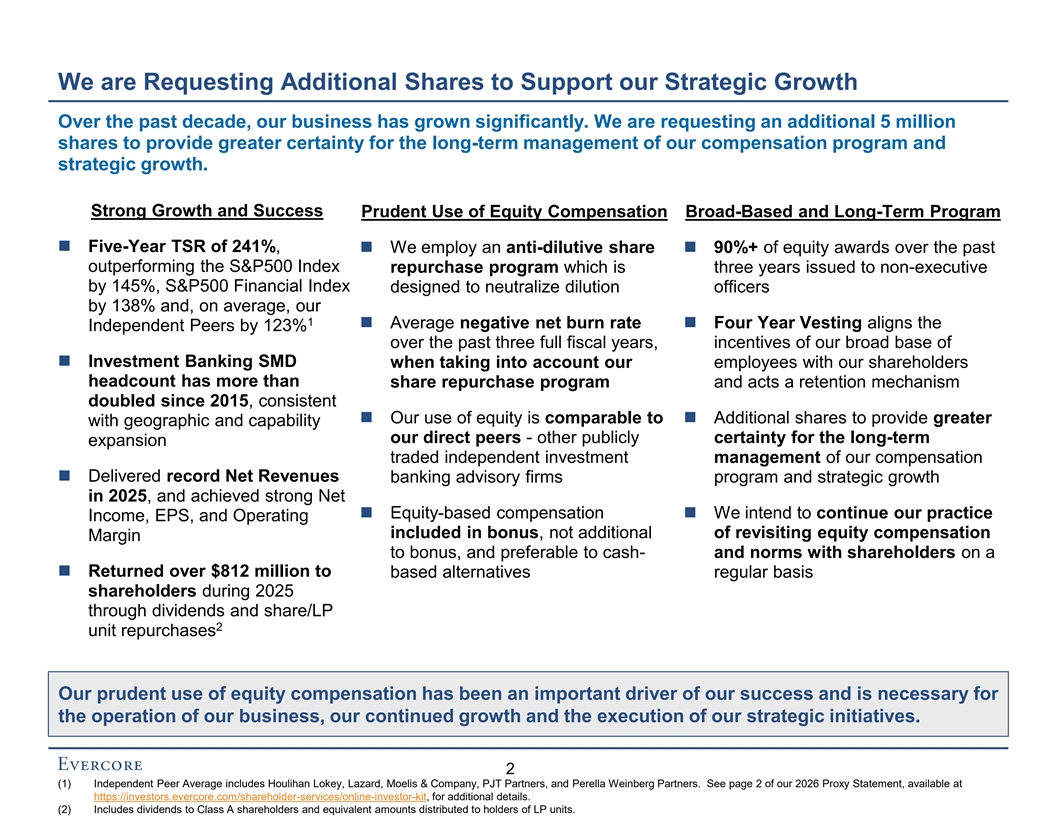

We are Requesting Additional Shares to Support our Strategic Growth Over the past decade, our business has grown significantly. We are requesting an additional 5 million shares to provide greater certainty for the long-term management of our compensation program and strategic growth. Strong Growth and Success Prudent Use of Equity Compensation Broad-Based and Long-Term Program ◼ Five-Year TSR of 241%, ◼ We employ an anti-dilutive share ◼ 90%+ of equity awards over the past outperforming the S&P500 Index repurchase program which is three years issued to non-executive by 145%, S&P500 Financial Index designed to neutralize dilution officers by 138% and, on average, our 1 ◼ Average negative net burn rate ◼ Four Year Vesting aligns the Independent Peers by 123% over the past three full fiscal years, incentives of our broad base of ◼ Investment Banking SMD when taking into account our employees with our shareholders headcount has more than share repurchase program and acts a retention mechanism doubled since 2015, consistent ◼ Our use of equity is comparable to ◼ Additional shares to provide greater with geographic and capability our direct peers - other publicly certainty for the long-term expansion traded independent investment management of our compensation ◼ Delivered record Net Revenues banking advisory firms program and strategic growth in 2025, and achieved strong Net ◼ Equity-based compensation ◼ We intend to continue our practice Income, EPS, and Operating included in bonus, not additional of revisiting equity compensation Margin to bonus, and preferable to cash- and norms with shareholders on a ◼ Returned over $812 million to based alternatives regular basis shareholders during 2025 through dividends and share/LP 2 unit repurchases Our prudent use of equity compensation has been an important driver of our success and is necessary for the operation of our business, our continued growth and the execution of our strategic initiatives. 2 (1) Independent Peer Average includes Houlihan Lokey, Lazard, Moelis & Company, PJT Partners, and Perella Weinberg Partners. See page 2 of our 2026 Proxy Statement, available at https://investors.evercore.com/shareholder-services/online-investor-kit, for additional details. (2) Includes dividends to Class A shareholders and equivalent amounts distributed to holders of LP units.

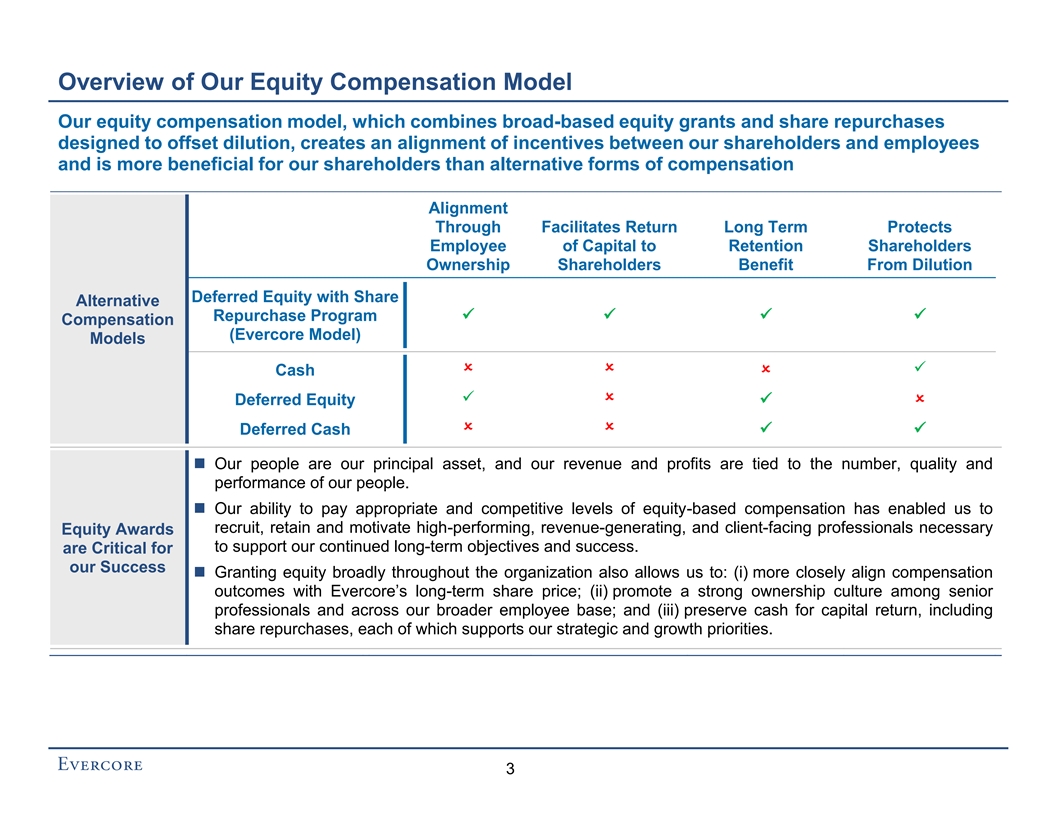

Overview of Our Equity Compensation Model Our equity compensation model, which combines broad-based equity grants and share repurchases designed to offset dilution, creates an alignment of incentives between our shareholders and employees and is more beneficial for our shareholders than alternative forms of compensation Alignment Through Facilitates Return Long Term Protects Employee of Capital to Retention Shareholders Ownership Shareholders Benefit From Dilution Deferred Equity with Share Alternative Repurchase Program ✓ ✓ ✓ ✓ Compensation (Evercore Model) Models O O ✓ O Cash ✓ O O Deferred Equity ✓ O O Deferred Cash ✓ ✓ û ◼ Our people are our principal asset, and our revenue and profits are tied to the number, quality and performance of our people. ◼ Our ability to pay appropriate and competitive levels of equity-based compensation has enabled us to recruit, retain and motivate high-performing, revenue-generating, and client-facing professionals necessary Equity Awards to support our continued long-term objectives and success. are Critical for our Success ◼ Granting equity broadly throughout the organization also allows us to: (i) more closely align compensation outcomes with Evercore’s long-term share price; (ii) promote a strong ownership culture among senior professionals and across our broader employee base; and (iii) preserve cash for capital return, including share repurchases, each of which supports our strategic and growth priorities. û û 3

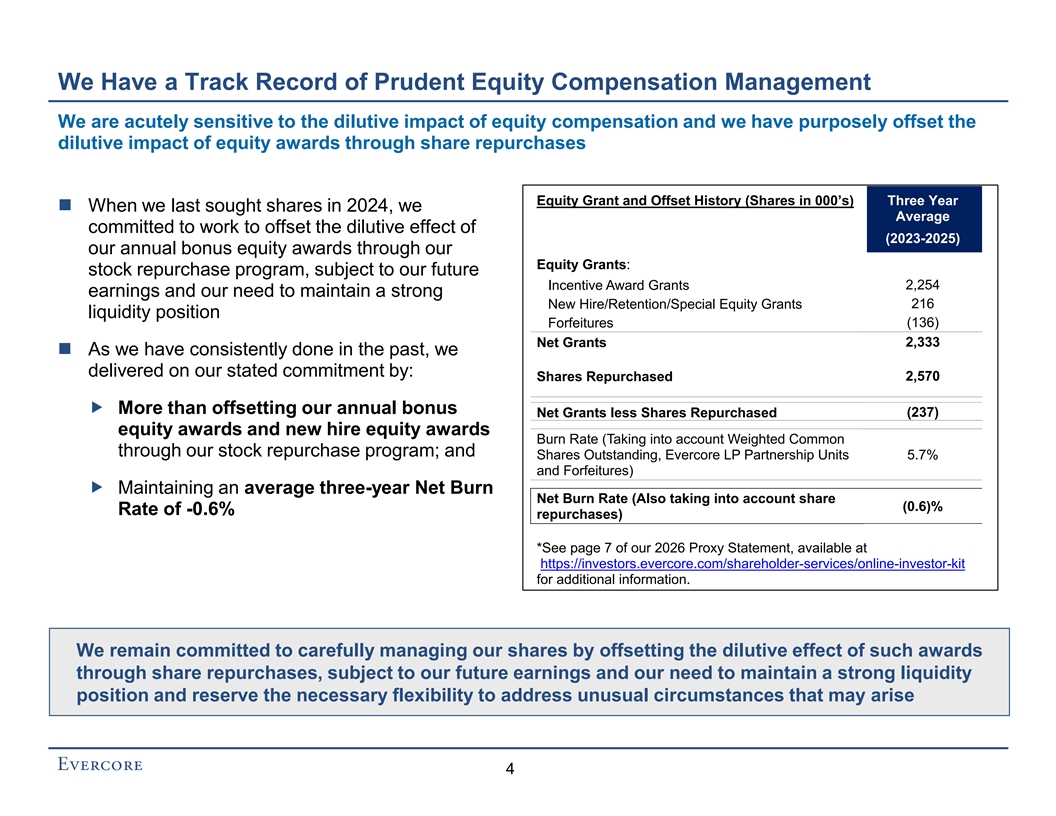

We Have a Track Record of Prudent Equity Compensation Management We are acutely sensitive to the dilutive impact of equity compensation and we have purposely offset the dilutive impact of equity awards through share repurchases Equity Grant and Offset History (Shares in 000’s) Three Year ◼ When we last sought shares in 2024, we Average committed to work to offset the dilutive effect of (2023-2025) our annual bonus equity awards through our Equity Grants: stock repurchase program, subject to our future 2,254 Incentive Award Grants earnings and our need to maintain a strong 216 New Hire/Retention/Special Equity Grants liquidity position Forfeitures (136) 2,333 Net Grants ◼ As we have consistently done in the past, we delivered on our stated commitment by: Shares Repurchased 2,570 „ More than offsetting our annual bonus Net Grants less Shares Repurchased (237) equity awards and new hire equity awards Burn Rate (Taking into account Weighted Common through our stock repurchase program; and Shares Outstanding, Evercore LP Partnership Units 5.7% and Forfeitures) „ Maintaining an average three-year Net Burn Net Burn Rate (Also taking into account share (0.6)% Rate of -0.6% repurchases) *See page 7 of our 2026 Proxy Statement, available at https://investors.evercore.com/shareholder-services/online-investor-kit for additional information. We remain committed to carefully managing our shares by offsetting the dilutive effect of such awards through share repurchases, subject to our future earnings and our need to maintain a strong liquidity position and reserve the necessary flexibility to address unusual circumstances that may arise 4

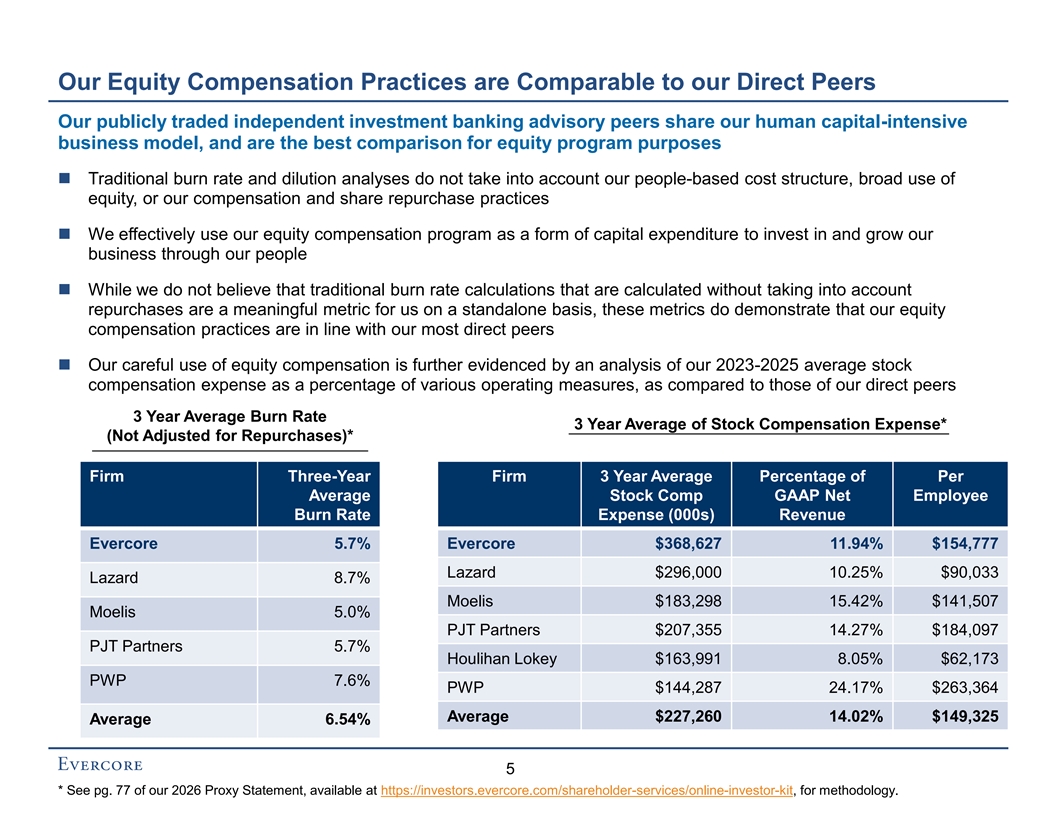

Our Equity Compensation Practices are Comparable to our Direct Peers Our publicly traded independent investment banking advisory peers share our human capital-intensive business model, and are the best comparison for equity program purposes ◼ Traditional burn rate and dilution analyses do not take into account our people-based cost structure, broad use of equity, or our compensation and share repurchase practices ◼ We effectively use our equity compensation program as a form of capital expenditure to invest in and grow our business through our people ◼ While we do not believe that traditional burn rate calculations that are calculated without taking into account repurchases are a meaningful metric for us on a standalone basis, these metrics do demonstrate that our equity compensation practices are in line with our most direct peers ◼ Our careful use of equity compensation is further evidenced by an analysis of our 2023-2025 average stock compensation expense as a percentage of various operating measures, as compared to those of our direct peers 3 Year Average Burn Rate 3 Year Average of Stock Compensation Expense* (Not Adjusted for Repurchases)* Firm Three-Year Firm 3 Year Average Percentage of Per Average Stock Comp GAAP Net Employee Burn Rate Expense (000s) Revenue Evercore 5.7% Evercore $368,627 11.94% $154,777 Lazard $296,000 10.25% $90,033 Lazard 8.7% Moelis $183,298 15.42% $141,507 Moelis 5.0% PJT Partners $207,355 14.27% $184,097 PJT Partners 5.7% Houlihan Lokey $163,991 8.05% $62,173 PWP 7.6% PWP $144,287 24.17% $263,364 Average $227,260 14.02% $149,325 Average 6.54% 5 * See pg. 77 of our 2026 Proxy Statement, available at https://investors.evercore.com/shareholder-services/online-investor-kit, for methodology.